Asset Retirement Obligation Rate Considerations In An Inflationary Market

This past year, the COVID pandemic has had a significant impact on our economy. We’ve seen supply disruptions, labor shortages, and increases in commodity prices that have combined to cause inflation to reach levels we haven’t seen since the late 1970s and early 1980s. As most companies start to close out their year-end financials, it’s important to take time to think through the impacts higher inflation can have on your Asset Retirement Obligation (ARO).

Typically, at year-end, oil and gas companies reassess the key inputs used to calculate their ARO liability: abandonment estimates, remaining life, working interests, as well as inflation and discount rates. While each of these inputs warrants discussion as they relate to a company’s policies, we’ll focus this discussion on how changes in the inflation rate used can impact a company’s liability and some considerations for when we’re in a period of increasing inflation.

How Inflation Rates Factor Into An ARO Calculation

The inflation rate is a key component in forecasting the expected future cash flow that will be required to abandon an asset. The abandonment estimate in today’s dollars is inflated using the supplied rate for the expected life of the asset to calculate that expected future value amount. That future value is then discounted back at the supplied discount rate to establish the current liability estimate.

READ MORE: The Benefits Of Asset Retirement Obligation (ARO) Software

When selecting an inflation rate to use in the calculation, it’s important to keep in mind that the ARO calculation is a long-term-view calculation; we’re trying to forecast the amount required to perform an activity that won’t be performed for upwards of 40 to 50 years in the future. Thus, we recommend using an inflation rate that considers the estimated life of the asset. It’s also important that the supporting documentation of the inflation rate is stated as management’s estimate and that the reasonableness of the estimate is supported by comparing it to the average inflation rate. By taking an average inflation rate that is roughly in line with the life of the assets for which we’re establishing liability, we create a liability that accounts for the fluctuations of interest rates over the life of the asset.

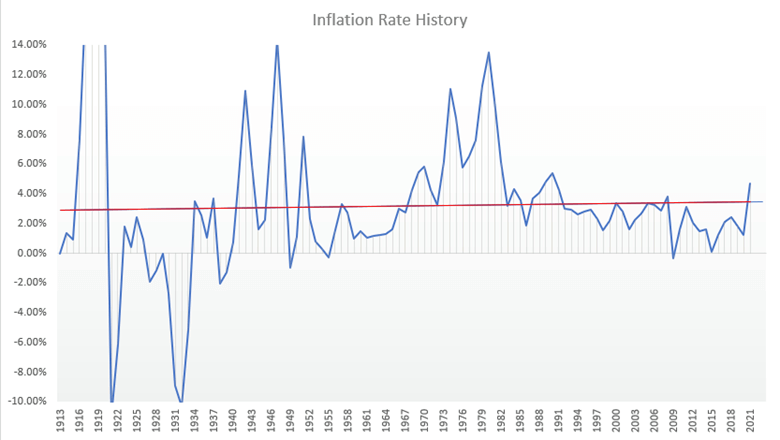

At year-end, the general practice is to use the prior year’s average to forecast forward. Depending on the index that is used, the inflation at the end of December 2021 is approximately 7.0%. While this may be an accurate picture of the economy currently, we recommend not just looking at the last year, but taking an average as it correlates to the lives of your assets. For example, if the average life of your assets is 30 years, use an average of the inflation rates over the last 30 years. We want to recognize the current increase in rates while still acknowledging that we’re trying to time an expenditure that won’t happen for another 30 plus years.

When we look at the inputs that are responsible for calculating the ARO liability (i.e., abandonment cost, life, working interest, inflation, and discount rate), all of them, except for working interest, are based on estimates. It’s important to put the imprecise nature of the overall calculation in context since each of these estimates is an educated guess. We are forecasting an expected cash flow by taking our best estimates today and projecting that forward, and the best indicator of what will happen in the future can be found by looking backward into the history of inflation. When we look back on the historical trends for inflation rates, we see periods of higher and lower inflation, but when averaged out, rates stay consistent.

READ MORE: 3 Ways ARO Software Can Improve Your Business

One might ask, “What’s the drawback of using today’s higher inflation rate?” One of the nuances of the US GAAP ASC 410-20 standard is that once a liability is established, only the incremental adjustments to the liability are recognized and captured as a layer. This creates a scenario where historical estimates continue until the liability is removed or the calculation is reset in a fresh start accounting scenario. The drawback to this practice of using a current inflation rate, instead of a long-term average, is that if the inputs used in the calculation are outside of the historical trends, the impact of that temporary condition will continue to impact the liability for years to come, long after that period has passed. We must realize that while current inflation rates are going up, they will most likely come down again in the future.

Looking at the chart above, we can correlate wide swings in inflation rates to major historical events; however, even with those large fluctuations, there’s a consistent average, as demonstrated by the red trendline above. In 2009, when we were in a deflation period, it would not be reasonable to expect a future expenditure to cost less 30 years later than it did in 2009. Therefore, we recommend using an inflation average loosely tied to the length of the life of your asset to ensure the most accurate liability estimate possible for this future-value calculation.

Related Insights

Our experts are here

for you.

When you choose Opportune, you gain access to seasoned professionals who not only listen to your needs, but who will work hand in hand with you to achieve established goals. With a sense of urgency and a can-do mindset, we focus on taking the steps necessary to create a higher impact and achieve maximum results for your organization.

LeadershipGeneral Contact Form

Looking for expertise in the energy industry? We’ve got you covered.

Find out why the new landmark legislation should provide a much-needed boost for the development of carbon capture.