Why Are E&Ps Slow To Respond To Higher Oil Prices?

Over the last several months (and right up to today) some of the headlines published in various media outlets have addressed the slower-than-expected response of operators to increase drilling activity as oil prices have risen. This appears to be consistent with the expectations of their equity investors and the realities of the tougher underwriting standards in the debt markets. Let’s look back at recent oil price spikes to compare the current rig count response to earlier ones.

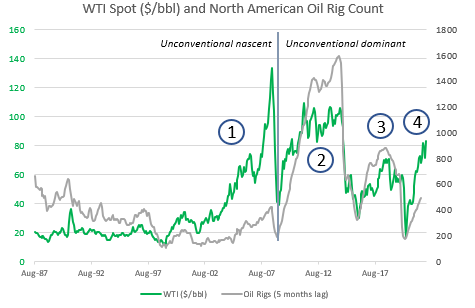

The graph below shows the average monthly WTI spot price and the average monthly North American oil-directed rig count from August 1987 to January 2022. The data are from the U.S. Energy Information Administration (EIA) and Baker Hughes, and the rig count has been shifted backward five months to account for the typical lag in the rig count response.

I’ve highlighted a few areas of the history.

- This was the period before unconventional oil production had taken off. New oil developments in the U.S. were typically offshore, many in the deepwater. These projects have long lead times and require an expectation that prices will remain high for a significant period. As a result, the big increase in oil prices from 2004-2007 didn’t result in much of an increase in the rig count. It probably resulted in a material increase in capital spending, however, since deepwater exploration and development is so expensive.

- This is the first price spike during what I’ve called the “unconventional dominant” period, and the rig activity response is exactly what we would expect. Since the nature of unconventional drilling allows for rapid development and the time to get wells on production is short, operators responded to capitalize on higher near-term prices. The resulting increase in production led to oversupply (which OPEC+ was unwilling to underwrite), so prices dropped, and the rig count quickly followed, which set the stage for the next cycle.

- As prices moved back into the $50-$60/bbl range, the rig count again responded rapidly and significantly until the pandemic depressed demand. This led to lower prices, and once again, the rig count quickly fell.

- The muted response in this period is evident. During the previous two cycles, oil prices above $80/bbl resulted in oil-directed rig counts of around 1,000 rigs, but right now we’re only at around 500.

Oil prices at the current levels are something of an outlier and it seems reasonable to expect a supply response. The big question is: who will make it? OPEC+ or U.S. operators? Investor expectations are only part of the reason for the slow response. U.S. labor markets are tight, many workers are wary of returning to the upstream business after the last downturn, and even frac sand is in tight supply. My expectation is that the U.S. industry will respond, but more slowly than in the past, until capital and other constraints are resolved.

Related Insights

Our experts are here

for you.

When you choose Opportune, you gain access to seasoned professionals who not only listen to your needs, but who will work hand in hand with you to achieve established goals. With a sense of urgency and a can-do mindset, we focus on taking the steps necessary to create a higher impact and achieve maximum results for your organization.

LeadershipGeneral Contact Form

Looking for expertise in the energy industry? We’ve got you covered.

Find out why the new landmark legislation should provide a much-needed boost for the development of carbon capture.