Exploring Profit Interests: Accounting & Valuation Insights

Executives at both public and private companies commonly receive performance-based incentives. The objective is to link compensation closely to a firm's financial results. These performance-based incentives can take many forms. One method that has grown in popularity, especially when private equity is involved, is using profits interests. Profit interests allow a partnership or limited liability company (“LLC”) to give key employees a larger stake in appreciating firm value without necessarily giving the employees ownership stake to existing company assets. The ability to avoid dilution is appealing to existing owners of capital interests and contributes largely to the increasing popularity of issuing profits interest shares.

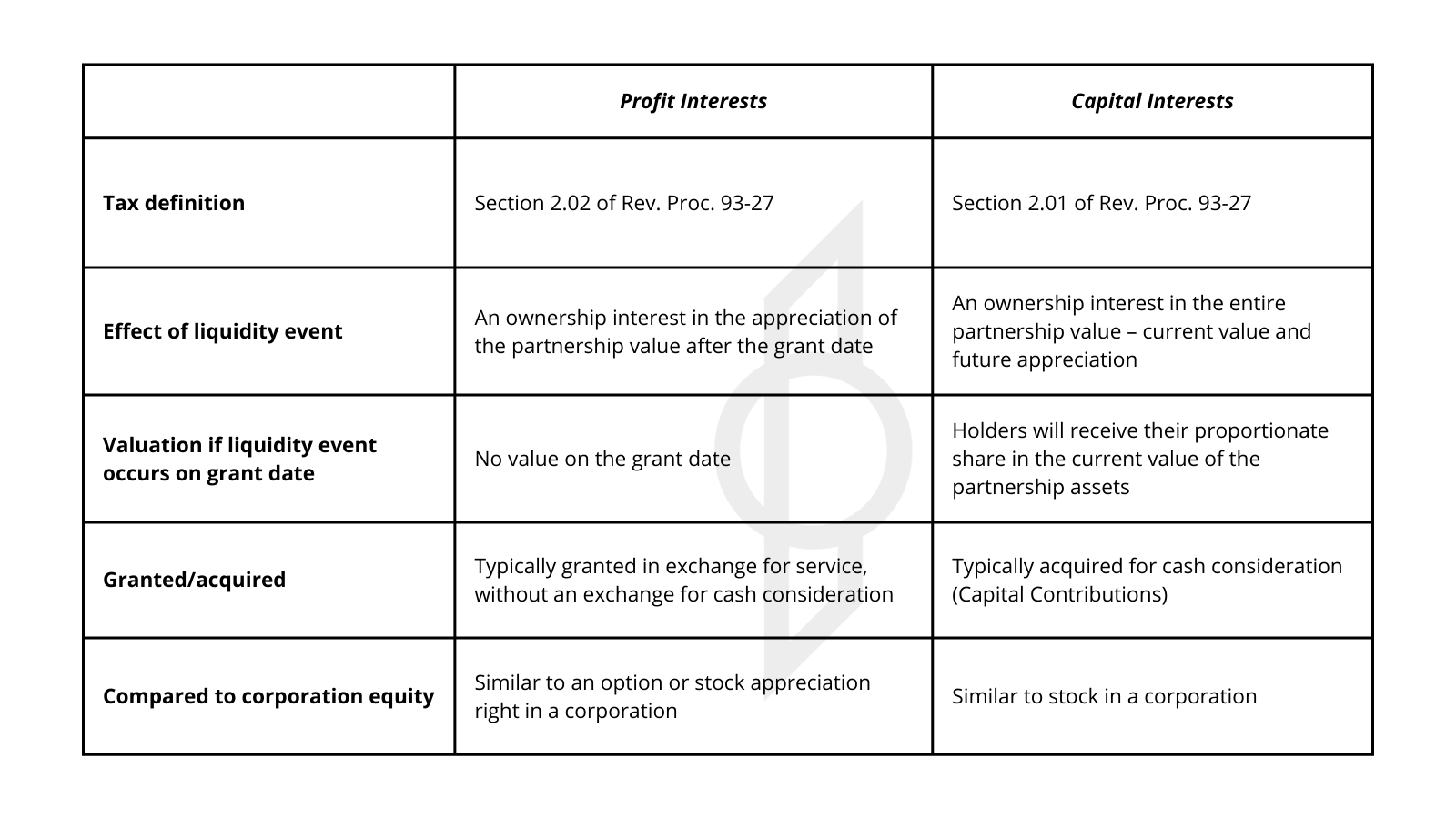

Understanding Profits Interests and Capital Interests

Profits interests and capital interests are the two major equity classes in a partnership (or LLC). Profit interests are partnership interests other than capital interests. Capital interests would give the holder a share of the proceeds if the partnership’s assets were sold at fair market value. Then, the proceeds were distributed in a complete liquidation of the partnership. The most important difference is that capital interests give a proportionate share of the entire partnership value, both current and future appreciation. In contrast, profits interests share only to the appreciation of a partnership value after the grant date.

Key differences between profits interests and capital interests:

Navigating Accounting Considerations

Depending on certain factors, profits interests may be accounted for as stock compensation under ASC Topic 718 or bonus or profit-sharing compensation under ASC Subtopic 710-10. When rights to the profits interest arrangement remain with the employee after termination of service, this would generally lead to accounting for them as stock compensation. This is because the retained value makes the profits interest behave like a unit of equity. On the other hand, when the rights to distributions from the arrangement are tied to continued employment and termination of employment gives little to no compensation for the forfeiture of the associated distribution rights, profits interests should be accounted for as a bonus or profit-sharing arrangement. The accounting application for profits interest arrangements can be quite complex and requires thorough knowledge of accounting standards.

Valuation Methods for Profits Interests

A valuation is required when profits interests are accounted for as stock compensation under ASC Topic 718. According to the 2013 AICPA Accounting and Valuation guide for the Valuation of Privately-Held-Company Equity Securities Issued as Compensation, the four most commonly used techniques in the valuation of equity securities are the Probability-Weighted Expected Return Method (“PWERM”), the Current Value Method (“CVM”), the Option Pricing Method (“OPM”) and the Hybrid Method, which combines the PWERM and OPM. The PWERM is usually not ideal for modeling profits interests because it is highly complex, requires many detailed assumptions that can be very subjective, and usually only considers a limited set of discrete outcomes rather than the entire range of possible outcomes. Furthermore, the complexity of the model makes it expensive and difficult to implement, and the limitation on possible outcomes is inadequate for valuing option-like payoffs such as those associated with profits interest arrangements. The CVM, based on current value only, does not consider the many variables that could change the value of a private company’s equity. For this reason, the CVM should only be used when the timing of a liquidity event is known with certainty or when a company is very early in its development. The OPM or Hybrid Method (a hybrid between PWERM and OPM) is the most appropriate method for valuing profits interest securities with option-like payoffs.

The OPM, most frequently using the Black-Scholes model, works by valuing the profits interests’ share in the future equity value above a threshold, similar to the way the model can value call options where the share price must rise above the strike price to have an intrinsic value above zero dollars. A major advantage of the OPM is that it can assign different strike prices based on liquidation preferences. The distribution order, as detailed in the LLC or Partnership agreement, determines the strike prices. The OPM makes it possible for profits interests to value a stake in only the appreciation of equity value beyond a given point or strike price.

Other valuation methods are also used to value option-like payoffs, two of which merit consideration when profits interests must be valued as equity-classified compensation. Monte Carlo simulation models can be used when profits interests receive value after a specific future event has occurred, such as reaching a threshold return on investment (“ROI”) or multiple on invested capital (“MOIC”). These simulation models incorporate uncertainty and various market factors through multiple iterations to see how uncertainty, on average, affects the expected equity value. Monte Carlo simulation models frequently use the Black-Scholes OPM model’s structure to determine the value for a specific class of equity.

Another valuation method frequently used to value profits interest, and other securities with option-like payoffs, is the backsolve method. The backsolve method in an OPM framework can infer the equity value implied by a recent financing transaction. This method involves solving for the total equity value of the enterprise such that the value of the most recent financing equals the amount paid (typically the per-unit price contributed by the sponsor in exchange for the capital interests) using assumptions developed for the expected term, volatility, and risk-free rate. This method is most dependable when the financing transaction is done at arm’s length, with both parties acting in their self-interest without pressure or undue duress from the counterparty. The resulting equity value is allocated through the distribution waterfall that flows through equity securities from high to low liquidation preference to arrive at the value for all securities within the enterprise, including profits interests.

Key Valuation Assumptions

Valuation assumptions for the company’s equity value, expected term, volatility, and discount for lack of marketability (“DLOM”) largely drive the valuation outcome. It is important to gather the necessary information to develop reliable estimates for these assumptions. Though it can take some time to gather, organize, and analyze the data required to make accurate predictions for these four factors, the valuation will only be as reliable as the assumptions.

The assumption for the total equity value as of the valuation date is a fundamental input to creating a reliable estimate for the value of various classes of equity. Profit interests are usually issued at the original transaction date when the private equity investment forms the capital interests. If this is true and the transaction is at arm’s length, the issue price of the capital interests can be used to backsolve for the value of the company’s equity on the issue date. However, if the valuation date is different from the issue date and there are no recent transactions from which the equity value can be implied, an enterprise valuation will need to be prepared to estimate the fair value of equity.

Ensuring Accuracy in Financial Reporting

With so many factors affecting which type of accounting to apply and how to value these profits interests, it can be daunting to ensure these securities are recorded in the financial statements in a manner that will not give cause for contest from auditors. Properly valuing all types of incentive units with option or option-like payoffs requires careful consideration of various elements.

Partnerships and companies often rely on trusted advisors to assist in navigating the complexities of incentive structures. These advisors help evaluate the potential long-term capital gain associated with profits interests, ensuring alignment with the company's objectives and the interests of its stakeholders. They also consider the impact of vesting schedules on employees and service partners, recognizing the significance of these incentives in attracting and retaining talent.

Ultimately, the goal is to provide clarity and confidence in valuing profits interests and other equity-based incentives. By leveraging expertise and industry knowledge, companies can effectively manage the complexities of incentive structures, enhancing their ability to attract, retain, and incentivize talent while maintaining stakeholder trust.

Related Insights

Our experts are here

for you.

When you choose Opportune, you gain access to seasoned professionals who not only listen to your needs, but who will work hand in hand with you to achieve established goals. With a sense of urgency and a can-do mindset, we focus on taking the steps necessary to create a higher impact and achieve maximum results for your organization.

LeadershipGeneral Contact Form

Looking for expertise in the energy industry? We’ve got you covered.

Find out why the new landmark legislation should provide a much-needed boost for the development of carbon capture.